What is ABC Analysis?

ABC analysis is the process of classifying the inventory into A, B and C classes based on their relative significance to business, either by their monetary value, utilization, carrying cost or any other factor. This allows leaders to allocate the company’s resources to maximize the efficiency.

Class A:

- Very important for an organization.

- High value, so tighter control, accurate records and frequent valuation required.

- Small (5-15) % of items account for Large (65-80) % of the value (consumption, costs, activity, etc.)

Class C:

- Is not critical for company’s operations.

- Comparatively low value so management will not lose sleep on the accuracy of inventory.

- Large (80+) % of items account for a relatively small (<15) % of the inventory value/consumption.

Class B:

- Essentially in between classes A and C.

- Value at par with quantity.

There is no fixed or globally followed percentage or factor. Every business can do it differently, and in fact with sophisticated ERP systems, can do the classification on multiple factors and report/track simultaneously.

How is ABC Analysis applied?

- Inventory planners can forecast the demand and manage the appropriate stock levels, in order to minimize carrying costs and avoid obsolete / low-demand (dead) stock.

- Companies can prioritize having quality trade agreements with suppliers on Class A items, at the best possible combined costs (item costs, shipping costs, services, quality, RMA, etc.).

- Optimize inventory by stocking up on popular/high-demand items and reducing stock of slow-moving items. Reducing the risk of running out of stock or plant slowdowns.

- Effective utilization of working capital.

- ABC classification can be applied to better understand the impact of price updates on margins.

- Continuous process improvements using periodic tracking and refinement of classification is important. The leadership can then prioritize resources for optimizing Class A items compared to doing the same for Classes B or C. For example, cycle counting.

- Enable informed stock replenishment decisions on changing the safety levels, etc.

Introduction to Inventory Control

Every business has a need to optimize their inventory and supply chain, and many times than not, it is a constant challenge. A proper inventory control helps organizations to manage the business uncertainties and fluctuations. Furthermore, as the cost of inventory is a sizable portion of working capital, organizations employ various inventory controlling techniques for effective utilization of available resources with minimal risk to business. In the advent of modern inventory control techniques, organizations can control the inventory better.

Applying such control techniques require vigor and most often being smart with classification of items, especially when dealing with hundreds to sometimes few thousands* of items. The inventory control techniques are applied selectively/discriminately to items. The inventory is classified based on its importance and specific inventory control is applied to each class, thus, optimizing the effort to manage large number of items.

*If you have few thousands of items, there is usually a better option to use item variants or dimensions, to optimize your item list.

The most common and very widely used classification is the ABC classification, to classify items based on its relative importance to business, i.e. based on monitory value, availability of resources and carrying cost.

The Law of Vital Few

ABC classification uses the Pareto’s principle, popularly known as ‘the 80–20 rule’, also referred as ‘the law of vital few’. The law states that for many events, roughly 80% of the effects come from 20% of causes. When applied to inventory, the same is interpreted as 20% of the items may account for 80% of total cost in the given period.

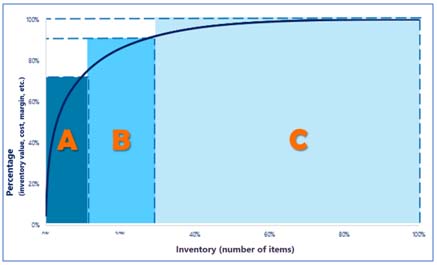

A sample diagram represents the classification of items based on inventory investment. It can be noted that 10% of items contribute to 70% of inventory investment, which is termed as the ‘significant few’ or otherwise called the A-class items. The next 20% of items that contribute the 20% of investment are termed as B-class items. The rest 70% of items, the major portion of items, contribute just 10% of inventory investment, which can be termed as the ‘insignificant many’ or C-class items. Thus, the classification provides the opportunity to apply different rigor but appropriate control techniques to respective class of items. While the A-class items deserve tightest control and most frequent review, B-class items can be put into medium level of control. C-class items can be managed through the simple rule of thumb. The sample used here is 70-20-10, and this ratio varies by organization.

Benefits of ABC Analysis

The classification of items into A, B& C yields many tangible and intangible benefits to the practicing organization.

- Smarter management of working capital: ABC analysis leads to a smarter management of working capital to manage optimal on-hand inventory and safety stocks, based on the consumption pattern and lead-times. Item replenishment policies can be derived from ABC analysis.

- Better Planning and forecasting: The ABC analysis help the planners to be more precise and effective in their demand and consumption forecasts.

- Wiser negotiations with vendors: With the insight of the vital few and insignificant many, negotiations with vendors become more wiser for price, lead time and delivery.

- Strategic pricing: Product pricing gets a shot in the arm as the analysis identifies the ‘vital few’ for profits and sales revenue. Marketing strategy and selling techniques could be revised based on the item classification to maximize revenue and profits.

- Optimized physical verification: Physical verification of stocks based on ABC classification helps organizations to effectively utilize organizational resources. While high value ‘vital few’ items could be checked more frequently, the low value ‘insignificant many’ can be checked seldom.

There is a flip side to ABC classification that skips the cost of shortage or the effect of an item going out of stock, which is managed through the VED (Vital, Essential, Desirable) analysis. Frequency of the movement of an item is omitted in ABC classification, which is covered under FSN (Fast, Slow, Non-moving) analysis.

How to use ABC classification?

ABC analysis is usually running on 4 different parameters/factors of an item namely item value, profit margin, sales revenue and item carrying cost.

| Type | Description |

| Value | Refers to the worth of an item in the inventory in monetary terms |

| Margin | Refers to the marginal income of an item in the inventory in monetary terms |

| Revenue | Refers to the sales revenue of an item in the inventory in monetary terms |

| Carrying cost | Refers to the period of the item that remains in inventory and its cost |

Let’s never forget that the ABC analysis works at its best only when it is ably supported by a standard inventory management solution. Dynamics 365*, the flagship Enterprise software (ERP) of Microsoft, has Supply Chain solution that helps organizations with end to end supply chain and inventory process (including the ABC classification), and integrated with the Finance solution for accounting and reporting.

*Dynamics 365 Finance & Supply Chain is integrated with Office 365, Azure Active Directory and Power Platform. The Power Platform allows for companies to automate their workflow and integrate data across all your systems (Power Automate), to extend the accessibility of the system/real-time data (Power Apps) and make informed and timely decisions(Power BI). All this is done in a highly secured and reliable cloud platform, and accessible on every device at your fingertips (literally).

Business case

A leading automobile parts manufacturing company faced the problem of out of stock items that either contributed to healthy margins or contributed to sizable revenue, few times a year. The company followed the policy to buy items based on requirements as the business operation faced the challenges of managing on-hand inventory. The history of tight control on all items had put unnecessary burden on the organization which resulted in loss of sales with not enough on-hand inventory. After some deliberation, the management went on to relax the control on inventory indiscriminately with no consideration for the relative value to the business. By this action the company systematically lost the control on the inventory management, and over a period the visibility of on-hand quantity and forecast reduced leading to out-of-stock often.

The management took actions to address the operational situation, when faced with stiff competition.

Solution offered by D365 Finance & Supply Chain

The ABC classification of item in D365 is handled in two (2) different ways. The classification process can either be a manual demarcation of items or by the statistical analysis by the system. Many decent ERP systems offer this feature these days, some more advanced/sophisticated than others.

Manual classification process

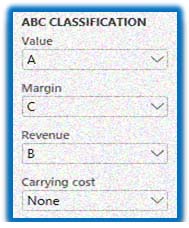

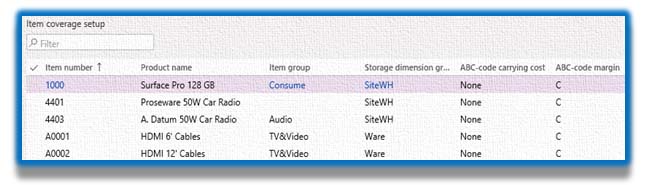

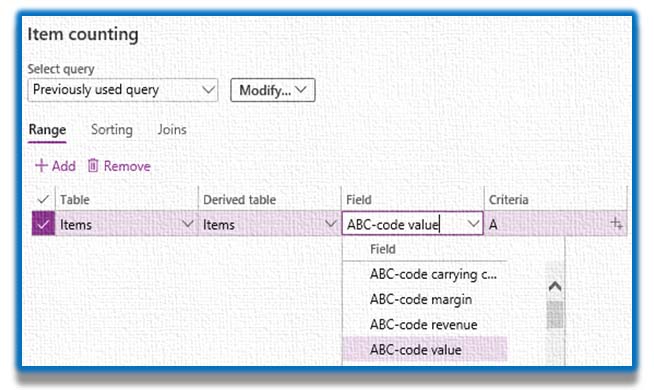

During new implementation cut-over process and in the case of new product introduction, system often falls short of historical data to calculate the ABC analysis. During such scenarios, instead of any statistical analysis, only predefined professional judgements are used to classify the item. The robust system feature allows users to manually classify items. An item can be classified on four different parameters such as value, margin, revenue and carrying cost as shown in the screen. Items can be assigned with specific category by selecting the category from the available options in the system.

While the manual classification is a good feature to start with the team’s knowledge, the nice feature in D365 lies in the statistical calculation executed by the system. The system uses ABC calculation to provide two different outputs, the first one is in the form a report and the second is an automatic update of item master with corresponding values.

ABC Classification Report

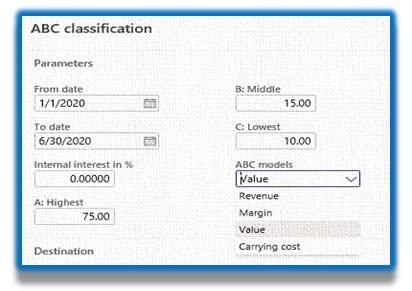

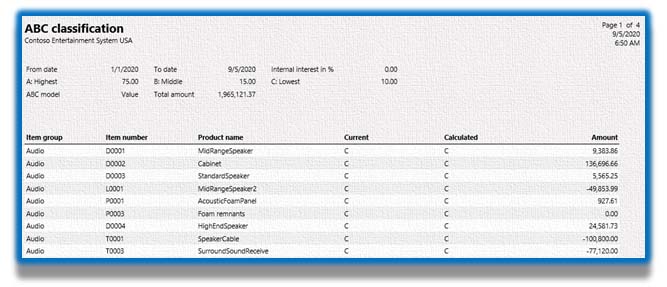

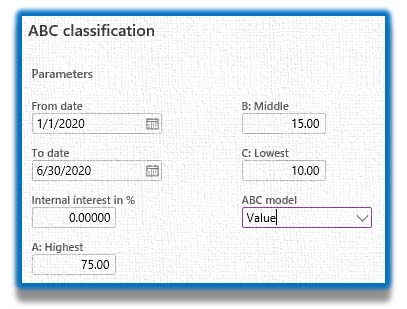

The report uses the system calculation logic to arrive at the ABC classification of items and the results are displayed in the form of a report. The beauty of the report is that the % split between A, B & C are user definable, for example, as 75%, 15% and 10% respectively. The ‘user-definable’ report parameter further helps the user to select the period of transaction to be considered for the calculation, to include % of interest that needs to be added and to select the model for calculation. The period selection would help to eliminate the outliers and use the transactions that would represent the business best. Business users can add the expected % of internal interest (IRR), which gets included in the calculation. The report can be run repeatedly for each of the ABC models, i.e. value, profit, revenue and carrying cost and with different parameter values.

Automatic Item Update

While the report helps to freeze the best parameter and result, the automatic update helps to update the item records directly with corresponding values of the ABC analysis. With a similar screen like the report, the parameter screen for the automatic update has the ‘user-definable’ fields for A, B, C percentage split, period selection, internal interest factor, and the ABC model for which the update has to be run.

When run with the parameters in place, items are updated automatically with corresponding classification for the selected model. As the item might fall under different classification on different models, the process can be repeated for others ABC models and the item master records are updated accordingly. The update can be run any number of times with no system limitations, but generally run according to the business needs on a periodic basis.

Inventory Control based on ABC Classification:

Applying the inventory control techniques post the ABC analysis in D365 is like standing on the shoulders of giants before us. The classification information can be pulled and used while applying checks and controls throughout inventory management. One such technique is the configuration of replenishment principles, item coverage. For example, all C- class items are put into an automatic purchase procedure with a reorder level (minimum quantities) and a maximum quantity to hold on stock.

Another inventory control technique where the classification is used is the item cycle counting, where items under class A is reviewed pretty frequently while class C items are counted on a less frequent basis and in most times selected for counting randomly.

This is an important topic discussed in many inventory management and board meetings, more so now than before with the supply chain and operational challenges companies are facing all over the globe.